Forecasting#

Importing Libraries and Dataset#

import pandas as pd

import matplotlib.pyplot as plt

# import seaborn as sns

import numpy as np

from statsmodels.tsa.holtwinters import ExponentialSmoothing

from collections import defaultdict

from statsmodels.tsa.arima.model import ARIMA

from statsmodels.tsa.statespace.sarimax import SARIMAX

from sklearn.metrics import mean_absolute_error

import warnings

import random

import xgboost as xgb

from prophet import Prophet

import os

import json

df = pd.read_csv('../../Stationary/Data/walmart.csv')

def cleaning(df_copy: pd.DataFrame) -> pd.DataFrame:

df = df_copy.copy(deep=True)

df['Date'] = pd.to_datetime(df['Date'], format=r"%d-%m-%Y")

df['Store'] = df['Store'].astype(pd.StringDtype()).astype('category')

df['Holiday_Flag'] = df['Holiday_Flag'].astype(pd.BooleanDtype())

df = df.rename(columns={col: col.lower() for col in df.columns})

return df

df = cleaning(df)

Methodology#

Data#

Source:

The data for this analysis is from Kaggle.Content:

The dataset contains weekly sales for 45 Walmart stores covering the years 2010 to 2012.Forecasting Strategy:

Since sales patterns differ across stores, forecasts will be developed separately for each store.

Modeling#

The following models were explored for forecasting:

Holt-Winters Exponential Smoothing

ARIMA

ARIMAX

SARIMA

SARIMAX

FB Prophet

XGBoost

Training#

Data Length:

Each store has 143 weeks of sales data. Our goal is to generate forecasts for the next 12 weeks.Hold-Out Period:

The last 12 weeks are set aside as a hold-out “forecast” period.Training and Validation Split:

The remaining 131 weeks are used for model development. To capture seasonal effects—especially because of yearly patterns—the first 105 weeks (over 2 full years) serve as our initial training set. The following 26 weeks are used as a validation period.Model Development:

For time series models (ARIMA, SARIMA, and SARIMAX), we train multiple candidate models with different orders on the 105-week training data. Information criteria (Akaike Information Criterion, AIC) are used to choose the best orders for each of these models.

For XGBoost and FB Prophet, several hyperparameter configurations (e.g., max depth, learning rate, changepoint sensitivity) are initially considered, but we do not use AIC/BIC for these models.

Evaluation#

Metric:

Although each model optimizes its own internal loss, we use Mean Absolute Error (MAE) as our common metric to compare performance.Growing Window Forecasting:

For the 26-week validation period, we simulate a real-world forecasting scenario using a growing window approach. Specifically:The model predicts one week ahead.

After each prediction, the actual value is added to the training set.

This process repeats until forecasts have been made for the entire 26-week period.

Model Selection:

The candidate model with the lowest average MAE over the validation windows is chosen as the best model.Final Forecast:

Once the best model is identified, it is re-trained on the full 131 weeks (the original training plus validation periods). Finally, this retrained model is used to forecast the reserved 12 weeks.

Different models#

Holt Winters i.e. Triple Exponential Smoothing

ARIMA with orders

(6, 1, 4)

(6, 1, 5)

(6, 2, 4)

(6, 2, 5)

(9, 2, 4)

(9, 2, 5)

SARIMA with orders

(6, 1, 4), (2, 1, 5, 52)

(6, 1, 5), (2, 1, 5, 52)

(6, 2, 4), (2, 1, 5, 52)

(6, 2, 5), (2, 1, 5, 52)

(9, 2, 4), (2, 1, 5, 52)

(9, 2, 5), (2, 1, 5, 52)

SARIMAX with cpi, holiday_flag and orders

(6, 1, 4), (2, 1, 5, 52)

(6, 1, 5), (2, 1, 5, 52)

(6, 2, 4), (2, 1, 5, 52)

(6, 2, 5), (2, 1, 5, 52)

(9, 2, 4), (2, 1, 5, 52)

(9, 2, 5), (2, 1, 5, 52)

XGBoost with

month

year

holiday_flag

CPI

lagged sales

FB Prophet

Saving and/or loading previous results#

Show code cell source

def custom_encoder(o):

"""

Custom encoder that converts non-serializable objects into a

serializable format with type markers. Now handles NumPy arrays,

tuples, and pandas Timestamp objects.

"""

if isinstance(o, np.ndarray):

return {"__ndarray__": o.tolist()}

if isinstance(o, tuple):

return {"__tuple__": list(o)}

if isinstance(o, pd.Timestamp):

return {"__pdtimestamp__": o.isoformat()}

raise TypeError(f"Object of type {type(o)} is not JSON serializable")

def custom_decoder(d):

"""

Checks for type markers in the dictionary and converts them back

to their original types. Now converts the pandas Timestamp marker

back to a pd.Timestamp object.

"""

if "__ndarray__" in d:

return np.array(d["__ndarray__"])

if "__tuple__" in d:

return tuple(d["__tuple__"])

if "__pdtimestamp__" in d:

return pd.Timestamp(d["__pdtimestamp__"])

return d

def load_all_results(file_path="results.json"):

"""

Loads the full results dictionary from file using custom_decoder.

If the file does not exist, returns an empty dictionary.

"""

if os.path.exists(file_path):

with open(file_path, "r") as file:

data = json.load(file, object_hook=custom_decoder)

return data

return {}

def save_all_results(results, file_path="results.json"):

"""

Saves the full results dictionary to file using custom_encoder.

"""

with open(file_path, "w") as file:

json.dump(results, file, default=custom_encoder, indent=4)

Train, Test and Eval split#

# Get sorted unique dates

unique_dates = sorted(df['date'].unique())

total_weeks = len(unique_dates)

# Reserve final 12 weeks for hold-out (final forecast)

holdout_dates = unique_dates[-12:]

# The remaining weeks (training + validation): should be total_weeks - 12.

train_val_dates = unique_dates[:-12]

# Split the 131 weeks: the first 105 weeks for training and the next 26 weeks for validation

train_dates = train_val_dates[:105]

val_dates = train_val_dates[105:]

Loss metric#

Data Preparation#

# Get the unique store identifiers (assuming 'store' is categorical)

stores = df['store'].cat.categories.tolist()

# Create a results dictionary to store individual store results, and later aggregated metrics

results = load_all_results()

# We will forecast in 2-week horizons over the 26 validation weeks.

forecast_horizon = 1

n_forecast_iterations = len(val_dates) // forecast_horizon # should be 26/2 = 13

Model Training#

Holt Winters#

Training#

Show code cell source

if 'HoltWinters' not in results:

results['HoltWinters'] = {

"store_results": {},

"aggregated_metrics": {}

}

# Loop over each store

for store in stores:

# Filter the store’s data and sort it by date.

store_df = df[df['store'] == store].sort_values('date').reset_index(drop=True)

# Split the store data into training and validation sets based on date.

train_store_df = store_df[store_df['date'].isin(train_dates)]

valid_store_df = store_df[store_df['date'].isin(val_dates)]

# Extract the weekly sales series (using 'date' as index)

train_series = train_store_df.set_index('date')['weekly_sales']

# Initialize lists to collect forecasts and actual values as we do a growing-window forecast.

store_predictions = []

store_actuals = []

forecast_dates_list = []

# Start with the training series; as we move forward, this will grow.

series_gw = train_series.copy()

# Iterate over each 2-week forecast window

for i in range(n_forecast_iterations):

# Fit the Holt–Winters (triple exponential smoothing) model:

# We assume an additive trend and additive seasonal component with season_length 52.

with warnings.catch_warnings():

warnings.filterwarnings("ignore")

model = ExponentialSmoothing(

series_gw,

trend="add",

seasonal="add",

seasonal_periods=52,

initialization_method="estimated",

)

fit = model.fit(optimized=True, remove_bias=True, use_brute=True)

# Forecast the next 'forecast_horizon' weeks

forecast = fit.forecast(forecast_horizon)

# Determine the forecast dates from our validation dates.

# For each iteration, select the next 2 weeks in order.

fc_start = i * forecast_horizon

fc_end = (i + 1) * forecast_horizon

fc_dates = val_dates[fc_start:fc_end]

# Get the actual weekly sales for the forecast dates from the validation set.

valid_series = valid_store_df.set_index('date')['weekly_sales']

actual = valid_series.loc[fc_dates]

# Append these forecasts and actuals to our lists.

store_predictions.extend(forecast.values)

store_actuals.extend(actual.values)

forecast_dates_list.extend(fc_dates)

# Update the growing window: as if we received these observations.

# (Using pd.concat instead of .append to avoid deprecation warnings.)

series_gw = pd.concat([series_gw, actual]).sort_index()

# After finishing the growing window forecast, compute rmse for the store.

store_predictions = np.array(store_predictions).tolist()

store_actuals = np.array(store_actuals).tolist()

store_mae = float(mean_absolute_error(store_actuals, store_predictions))

# Save results for this store.

results['HoltWinters']['store_results'][store] = {

'forecast_dates': forecast_dates_list,

'predictions': store_predictions,

'actuals': store_actuals,

'mae': store_mae

}

Calculate Errors#

all_mae = []

for store in stores:

store_mae = results['HoltWinters']['store_results'][store]['mae']

all_mae.append(store_mae)

avg_mae = float(np.mean(all_mae))

std_mae = float(np.std(all_mae))

results['HoltWinters']['aggregated_metrics'] = {

'avg_mae': avg_mae,

'std_mae': std_mae

}

pd.Series(all_mae).describe()

count 45.000000

mean 42961.345915

std 26876.922926

min 9307.971428

25% 23044.419884

50% 37918.606065

75% 59191.844352

max 126763.135885

dtype: float64

save_all_results(results)

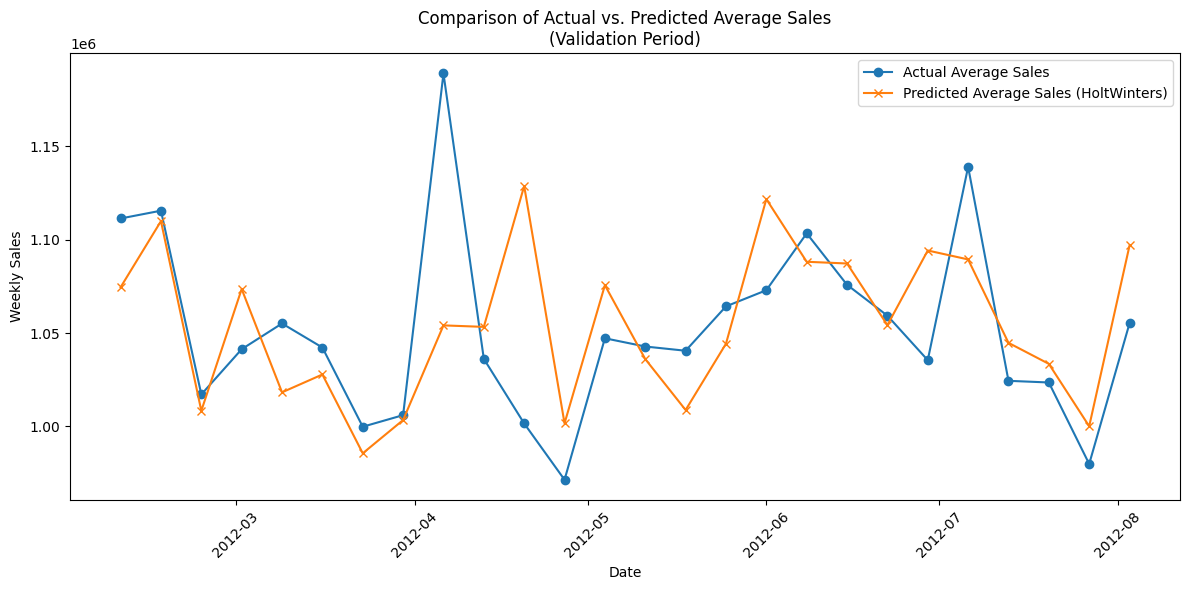

Visualize predictions#

Show code cell source

# Initialize dictionaries to aggregate forecast values by date.

pred_by_date = defaultdict(list)

actual_by_date = defaultdict(list)

# Loop through each store's results

for store in stores:

store_result = results['HoltWinters']['store_results'][store]

for dt, pred, actual in zip(store_result['forecast_dates'],

store_result['predictions'],

store_result['actuals']):

# Convert dt into a pd.Timestamp (if not already)

dt = pd.to_datetime(dt)

pred_by_date[dt].append(pred)

actual_by_date[dt].append(actual)

# Sort the forecasted dates

sorted_dates = sorted(pred_by_date.keys())

# For each date, compute the average predicted and actual weekly sales.

avg_pred = [np.mean(pred_by_date[dt]) for dt in sorted_dates]

avg_actual = [np.mean(actual_by_date[dt]) for dt in sorted_dates]

# Plot the actual vs. predicted average sales

plt.figure(figsize=(12, 6))

plt.plot(sorted_dates, avg_actual, marker='o', label='Actual Average Sales')

plt.plot(sorted_dates, avg_pred, marker='x',

label='Predicted Average Sales (HoltWinters)')

plt.xlabel("Date")

plt.ylabel("Weekly Sales")

plt.title("Comparison of Actual vs. Predicted Average Sales\n(Validation Period)")

plt.legend()

plt.xticks(rotation=45)

plt.tight_layout()

plt.show()

ARIMA#

Training#

results = load_all_results()

Show code cell source

if 'ARIMA' not in results:

results['ARIMA'] = {

"store_results": {},

"aggregated_metrics": {}

}

# Define candidate ARIMA orders to consider

candidate_orders = [(6, 1, 4), (6, 1, 5), (6, 2, 4), (6, 2, 5)]

# Get unique stores (assuming the store column is categorical)

stores = df['store'].cat.categories.tolist()

# Loop over each store

for store in stores:

# Filter the store’s data and sort by date

store_df = df[df['store'] == store].sort_values('date').reset_index(drop=True)

# Split the data into training and validation based on date.

train_store_df = store_df[store_df['date'].isin(train_dates)]

valid_store_df = store_df[store_df['date'].isin(val_dates)]

# Extract the weekly sales series from training data.

train_series = train_store_df.set_index('date')['weekly_sales']

# First, determine the best ARIMA order by fitting each candidate on just the

# training portion (105 weeks) and comparing their AIC.

best_aic = np.inf

best_order = None

aic_bic = pd.DataFrame(columns=['order', 'aic', 'bic'], index = list(range(len(candidate_orders))))

for idx, order in enumerate(candidate_orders):

try:

# Suppress warnings during the ARIMA fitting

with warnings.catch_warnings():

warnings.filterwarnings("ignore")

model = ARIMA(train_series, order=order)

fit_model = model.fit()

aic_bic.iloc[idx]['order'] = order

aic_bic.iloc[idx]['aic'] = fit_model.aic

aic_bic.iloc[idx]['bic'] = fit_model.bic

# print(f"For store {store}, order {order}, AIC: {fit_model.aic}, BIC: {fit_model.bic}")

if fit_model.aic < best_aic:

best_aic = fit_model.aic

best_order = order

except Exception as e:

print(f"Store {store}, order {order} failed: {e}")

continue

# Now, using the selected best_order, do a growing-window forecast on the

# 26-week validation set (forecasting 2 weeks at a time).

store_predictions = []

store_actuals = []

forecast_dates_list = []

# Start the growing window with the training series.

series_gw = train_series.copy()

# The number of forecast iterations (26 weeks / 2 per iteration).

n_forecast_iterations = len(val_dates) // forecast_horizon

for i in range(n_forecast_iterations):

try:

with warnings.catch_warnings():

warnings.filterwarnings("ignore")

model_gw = ARIMA(series_gw, order=best_order)

fit_gw = model_gw.fit()

forecast_result = fit_gw.forecast(steps=forecast_horizon)

except Exception as e:

print(f"Store {store}: Forecast iteration {i} failed with error: {e}")

# If forecasting fails, you can choose to assign missing values.

forecast_result = np.full(forecast_horizon, series_gw.iloc[-1])

# Identify the forecast dates (next 2 weeks from the validation list)

fc_start = i * forecast_horizon

fc_end = (i + 1) * forecast_horizon

fc_dates = val_dates[fc_start:fc_end]

# Get the actual values for these forecast dates

valid_series = valid_store_df.set_index('date')['weekly_sales']

actual = valid_series.loc[fc_dates]

# Append predictions, actuals, and forecast dates

store_predictions.extend(

forecast_result if isinstance(forecast_result, np.ndarray)

else forecast_result.tolist()

)

store_actuals.extend(actual.values)

forecast_dates_list.extend(fc_dates)

# Grow the training window with the actual observations just forecasted.

series_gw = pd.concat([series_gw, actual]).sort_index()

# After finishing the growing window forecast, compute rmse for the store.

store_predictions = np.array(store_predictions).tolist()

store_actuals = np.array(store_actuals).tolist()

store_mae = float(mean_absolute_error(store_actuals, store_predictions))

# Save results for this store.

results['ARIMA']['store_results'][store] = {

'best_order': best_order,

'forecast_dates': forecast_dates_list,

'predictions': store_predictions,

'actuals': store_actuals,

'mae': store_mae

}

Store 38: Forecast iteration 15 failed with error: LU decomposition error.

Calculate Errors#

all_mae = []

for store in stores:

store_mae = results['ARIMA']['store_results'][store]['mae']

all_mae.append(store_mae)

avg_mae = float(np.mean(all_mae))

std_mae = float(np.std(all_mae))

results['ARIMA']['aggregated_metrics'] = {

'avg_mae': avg_mae,

'std_mae': std_mae

}

pd.Series(all_mae).describe()

count 45.000000

mean 55857.767171

std 31973.065994

min 8107.999214

25% 32722.058617

50% 50691.990753

75% 85070.740653

max 128366.846170

dtype: float64

save_all_results(results)

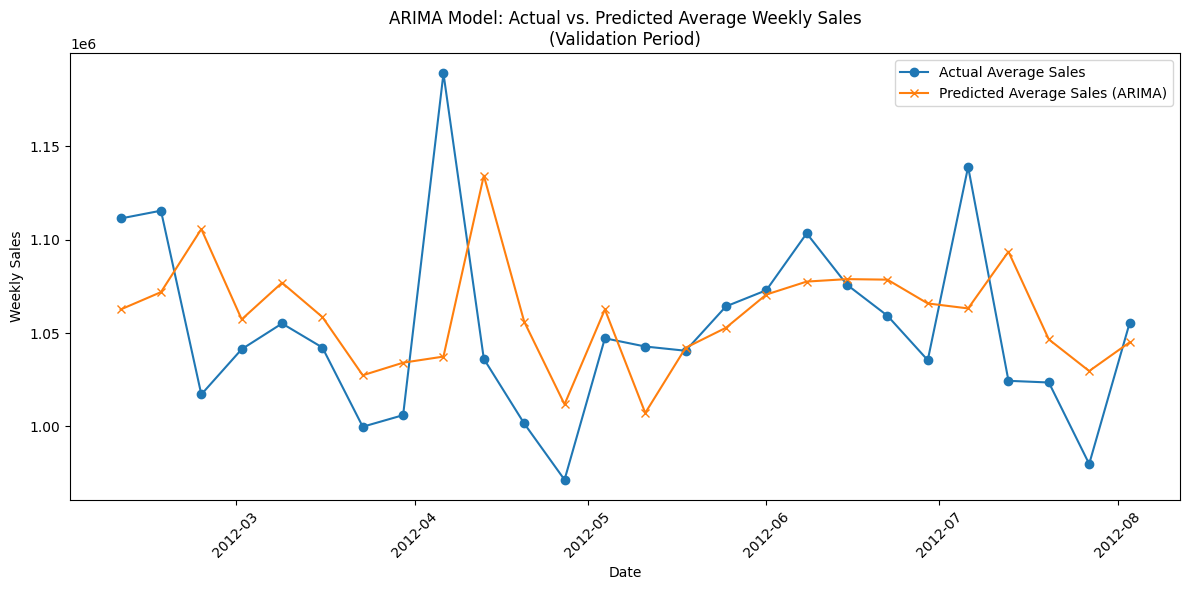

Visualize Predictions#

Show code cell source

# We'll collect forecasted predictions and actuals per date across all stores.

pred_by_date = defaultdict(list)

actual_by_date = defaultdict(list)

for store in stores:

store_result = results['ARIMA']['store_results'][store]

for dt, pred, act in zip(store_result['forecast_dates'],

store_result['predictions'],

store_result['actuals']):

dt = pd.to_datetime(dt)

pred_by_date[dt].append(pred)

actual_by_date[dt].append(act)

# Sort the forecasted dates

sorted_dates = sorted(pred_by_date.keys())

# Calculate the average predicted and actual sales across stores for each date.

avg_pred = [np.mean(pred_by_date[dt]) for dt in sorted_dates]

avg_actual = [np.mean(actual_by_date[dt]) for dt in sorted_dates]

# Plot the results

plt.figure(figsize=(12, 6))

plt.plot(sorted_dates, avg_actual, marker='o', label='Actual Average Sales')

plt.plot(sorted_dates, avg_pred, marker='x',

label='Predicted Average Sales (ARIMA)')

plt.xlabel("Date")

plt.ylabel("Weekly Sales")

plt.title("ARIMA Model: Actual vs. Predicted Average Weekly Sales\n(Validation Period)")

plt.legend()

plt.xticks(rotation=45)

plt.tight_layout()

plt.show()

XGBoost#

Separate train test split and growing windows#

# Split the 131 weeks: the first 105 weeks for training and the next 26 weeks for validation

train_dates = train_val_dates[:105]

val_dates = train_val_dates[105:]

# We will forecast in 4-week horizons over the 20 validation weeks.

forecast_horizon = 1

n_forecast_iterations = len(val_dates) // forecast_horizon # should be 20/2 = 10

Training#

Show code cell source

def create_features(df, lags=[1, 2], include_diffs=True):

df = df.copy()

df["month"] = df["date"].dt.month

df["year"] = df["date"].dt.year

df["holiday_flag_int"] = df["holiday_flag"].astype(int)

# Create lag features

for lag in lags:

df[f"sales_lag_{lag}"] = df["weekly_sales"].shift(periods = lag)

# Create difference features if required.

if include_diffs:

# First-order difference: difference between consecutive weekly_sales

df["sales_diff_1"] = df["weekly_sales"].diff(1)

# Second-order difference: difference of first differences (or equivalently

# the two-period difference)

df["sales_diff_2"] = df["weekly_sales"].diff(2)

# Drop rows with missing values due to lag / difference calculation.

df = df.dropna()

return df

Show code cell source

results = load_all_results()

if 'XGBoost' not in results:

results['XGBoost'] = {

"store_results": {},

"aggregated_metrics": {}

}

# Assume stores are available from the categorical 'store' column.

stores = df["store"].cat.categories.tolist()

# Define lag values. (These are used in addition to our newly added difference features.)

lag_features = [1, 2, 3, 4, 5, 6]

for store in stores:

# Filter and sort the data for the current store.

store_df = df[df["store"] == store].sort_values("date").reset_index(drop=True)

# Split the store's data into training (105 weeks) and validation (26 weeks).

train_store_df = store_df[store_df["date"].isin(train_dates)]

valid_store_df = store_df[store_df["date"].isin(val_dates)]

# Start the growing window with the training data.

data_gw = train_store_df.copy()

data_gw = data_gw.sort_values("date").reset_index(drop=True)

# Lists to hold forecasts/actuals for the current store.

store_predictions = []

store_actuals = []

forecast_dates_list = []

# Calculate the number of iterations based on the forecast horizon.

n_iter = len(val_dates) // forecast_horizon

for i in range(n_iter):

# --- TRAINING STEP ---

# Build the training features using the helper function (includes diffs).

train_feats = create_features(data_gw, lags=lag_features, include_diffs=True)

# Define the feature set.

# Calendar features, holiday_flag, CPI, lags, and differences.

X_train = train_feats[[

"month",

"year",

"holiday_flag_int",

"cpi",

"sales_lag_1",

"sales_lag_2",

"sales_lag_3",

"sales_lag_4",

"sales_lag_5",

"sales_lag_6",

"sales_diff_1",

"sales_diff_2"

]]

y_train = train_feats["weekly_sales"]

# Train the XGBoost model. Adjust hyperparameters as needed.

model = xgb.XGBRegressor(

objective="reg:squarederror",

n_estimators=50,

max_depth=5,

learning_rate=0.075,

random_state=42,

)

model.fit(X_train, y_train)

# --- FORECASTING STEP ---

# Determine forecast dates for the current window (next 2 weeks).

fc_start = i * forecast_horizon

fc_end = (i + 1) * forecast_horizon

fc_dates = val_dates[fc_start:fc_end]

fc_preds = []

for fc_date in fc_dates:

# Extract calendar and economic features from the validation set.

row = valid_store_df[valid_store_df["date"] == fc_date]

if row.empty:

continue

month = row["date"].dt.month.values[0]

year = row["date"].dt.year.values[0]

holiday_flag_int = int(row["holiday_flag"].values[0])

CPI_val = row["cpi"].values[0]

# --- Compute lag features from data_gw ---

# Ensure we have enough observations to compute both lag and difference features.

sales_lag_1 = data_gw["weekly_sales"].iloc[-1]

sales_lag_2 = data_gw["weekly_sales"].iloc[-2] #if len(data_gw) >= 2 else sales_lag_1

sales_lag_3 = data_gw["weekly_sales"].iloc[-3]

sales_lag_4 = data_gw["weekly_sales"].iloc[-4] #if len(data_gw) >= 2 else sales_lag_1

sales_lag_5 = data_gw["weekly_sales"].iloc[-3]

sales_lag_6 = data_gw["weekly_sales"].iloc[-4] #if len(data_gw) >= 2 else sales_lag_1

# Compute first difference feature

sales_diff_1 = sales_lag_1 - sales_lag_2

# For the second difference, we need the third most recent data point.

if len(data_gw) >= 3:

# sales_lag_3 = data_gw["weekly_sales"].iloc[-3]

sales_diff_2 = sales_lag_1 - 2 * sales_lag_2 + sales_lag_3

else:

sales_diff_2 = sales_diff_1 # Fallback if not enough data

# Construct a DataFrame for this forecast sample.

X_fc = pd.DataFrame({

"month": [month],

"year": [year],

"holiday_flag_int": [holiday_flag_int],

"cpi": [CPI_val],

"sales_lag_1": [sales_lag_1],

"sales_lag_2": [sales_lag_2],

"sales_lag_3": [sales_lag_3],

"sales_lag_4": [sales_lag_4],

"sales_lag_5": [sales_lag_5],

"sales_lag_6": [sales_lag_6],

"sales_diff_1": [sales_diff_1],

"sales_diff_2": [sales_diff_2],

})

# Generate the prediction for the current forecast date.

pred = model.predict(X_fc)[0]

fc_preds.append(pred)

# Append the predicted record to the growing window data.

# Some features (e.g., temperature/fuel_price/unemployment) may not be available.

new_row = pd.DataFrame({

"store": [store],

"date": [fc_date],

"weekly_sales": [row["weekly_sales"].values[0]],

"holiday_flag": [row["holiday_flag"].values[0]],

"temperature": [np.nan],

"fuel_price": [np.nan],

"cpi": [CPI_val],

"unemployment": [np.nan],

})

data_gw = pd.concat([data_gw, new_row], ignore_index=True)

data_gw = data_gw.sort_values("date").reset_index(drop=True)

# Get actual weekly_sales for these forecast dates.

actual_vals = []

for fc_date in fc_dates:

act_row = valid_store_df[valid_store_df["date"] == fc_date]

if act_row.empty:

continue

actual_vals.append(act_row["weekly_sales"].values[0])

store_predictions.extend(fc_preds)

store_actuals.extend(actual_vals)

forecast_dates_list.extend(fc_dates)

store_predictions = np.array(store_predictions).tolist()

store_actuals = np.array(store_actuals).tolist()

store_mae = float(mean_absolute_error(store_actuals, store_predictions))

# Save store results in the results dictionary.

results["XGBoost"]["store_results"][store] = {

"forecast_dates": forecast_dates_list,

"predictions": store_predictions,

"actuals": store_actuals,

"mae": store_mae,

}

Calculate Errors#

all_mae = []

for store in stores:

store_mae = results['XGBoost']['store_results'][store]['mae']

all_mae.append(store_mae)

avg_mae = float(np.mean(all_mae))

std_mae = float(np.std(all_mae))

results['XGBoost']['aggregated_metrics'] = {

'avg_mae': avg_mae,

'std_mae': std_mae

}

pd.Series(all_mae).describe()

count 45.000000

mean 71033.110247

std 42442.068225

min 10995.485433

25% 35036.849567

50% 63731.893462

75% 98883.153269

max 194336.745769

dtype: float64

save_all_results(results)

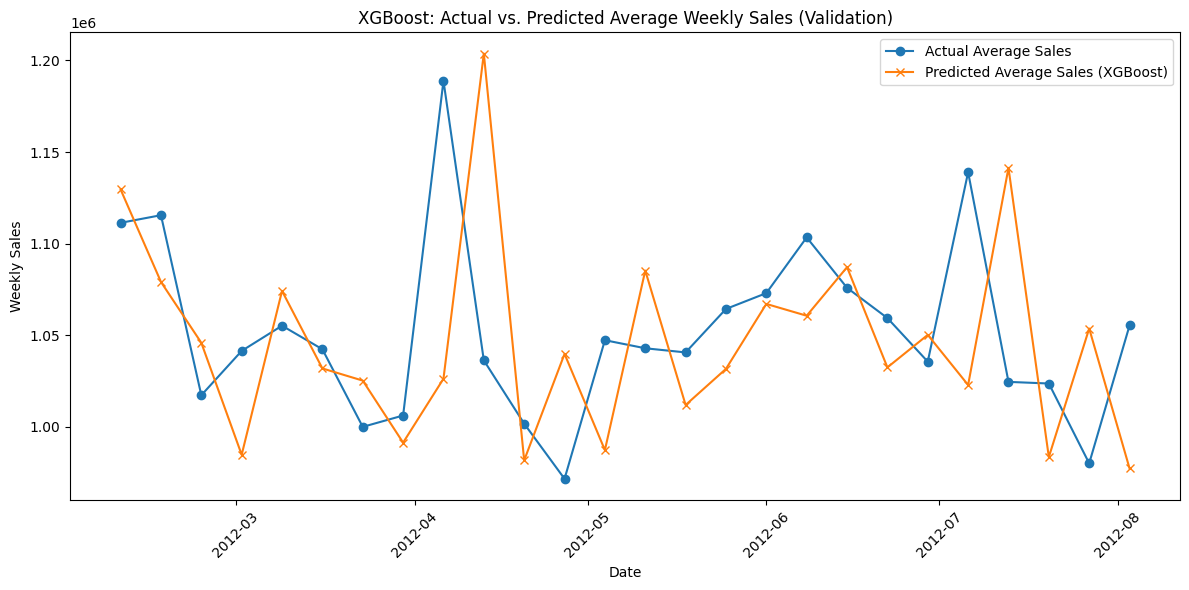

Visualize Predictions#

Show code cell source

pred_by_date = defaultdict(list)

actual_by_date = defaultdict(list)

for store in stores:

store_result = results["XGBoost"]["store_results"][store]

for dt, pred, act in zip(store_result["forecast_dates"],

store_result["predictions"],

store_result["actuals"]):

dt = pd.to_datetime(dt)

pred_by_date[dt].append(pred)

actual_by_date[dt].append(act)

# Sort the forecast dates and compute the average across stores.

sorted_dates = sorted(pred_by_date.keys())

avg_pred = [np.mean(pred_by_date[dt]) for dt in sorted_dates]

avg_actual = [np.mean(actual_by_date[dt]) for dt in sorted_dates]

plt.figure(figsize=(12, 6))

plt.plot(sorted_dates, avg_actual, marker="o", label="Actual Average Sales")

plt.plot(sorted_dates, avg_pred, marker="x", label="Predicted Average Sales (XGBoost)")

plt.xlabel("Date")

plt.ylabel("Weekly Sales")

plt.title("XGBoost: Actual vs. Predicted Average Weekly Sales (Validation)")

plt.legend()

plt.xticks(rotation=45)

plt.tight_layout()

plt.show()

FB Prophet#

Separate train test split and growing windows#

# Split the 131 weeks: the first 105 weeks for training and the next 26 weeks for validation

train_dates = train_val_dates[:105]

val_dates = train_val_dates[105:]

# We will forecast in 4-week horizons over the 20 validation weeks.

forecast_horizon = 1

n_forecast_iterations = len(val_dates) // forecast_horizon # should be 20/2 = 10

# random_stores = random.sample(stores, 25)

Training#

import logging

logging.getLogger("prophet").setLevel(logging.WARNING)

logging.getLogger("cmdstanpy").disabled=True

Show code cell source

# Initialize results dictionary for Prophet forecasts.

results = load_all_results()

if 'Prophet' not in results:

results['Prophet'] = {

"store_results": {},

"aggregated_metrics": {}

}

# Get the list of stores (assuming the store column is categorical).

stores = df["store"].cat.categories.tolist()

holidays = (

df[df['holiday_flag']][['date']] # select only rows where holiday_flag is True

.drop_duplicates() # remove duplicate dates if needed

.rename(columns={'date': 'ds'})

)

holidays['holiday'] = 'holiday' # Label each date with a name (could be more specific)

# Optionally, if you believe the effect spans extra days, add a window:

holidays['lower_window'] = -1 # The holiday's effect starts one day prior

holidays['upper_window'] = 1 # The effect lasts one day after

# Loop over each store.

for store in stores:

# --- Data Preparation for Prophet ---

# Filter the data for the current store and sort by date.

store_df = df[df["store"] == store].sort_values("date").reset_index(drop=True)

# Split store_df into training and validation based on your date lists.

train_store_df = store_df[store_df["date"].isin(train_dates)]

valid_store_df = store_df[store_df["date"].isin(val_dates)]

# Convert to Prophet's expected format: "ds" (for date) and "y" (for weekly_sales).

train_prophet = train_store_df[["date", "weekly_sales"]].rename(

columns={"date": "ds", "weekly_sales": "y"}

)

valid_prophet = valid_store_df[["date", "weekly_sales"]].rename(

columns={"date": "ds", "weekly_sales": "y"}

)

# Initialize lists to store forecasts, actuals, and the forecast dates.

store_predictions = []

store_actuals = []

forecast_dates_list = []

# Determine the number of forecast iterations (e.g., for 26 weeks with a 2-week horizon).

n_iter = len(valid_prophet) // forecast_horizon

valid_dates = valid_prophet["ds"].tolist() # these should already be sorted

# Growing-window forecast loop.

for i in range(n_iter):

# Initialize the Prophet model with appropriate parameters

model = Prophet(

growth="linear", # Use a linear trend.

changepoints=None, # Let Prophet automatically pick changepoints.

n_changepoints=25, # Default number of potential changepoints.

changepoint_range=0.8, # Use the first 80% of the history for changepoint detection.

yearly_seasonality=True, # Include yearly seasonality (important for holidays).

weekly_seasonality=False, # Include weekly seasonality (even for weekly data, if relevant).

daily_seasonality=False, # Daily seasonality is not applicable for weekly data.

holidays=holidays, # Pass in your holidays DataFrame.

seasonality_mode="additive", # Use an additive seasonality.

seasonality_prior_scale=10.0, # Default prior scale for seasonal effects.

holidays_prior_scale=10.0, # Default prior scale for holiday effects.

changepoint_prior_scale=0.05, # Controls the flexibility of trend changepoints.

mcmc_samples=0, # Use MAP estimation for faster fitting.

interval_width=0.80, # 80% prediction intervals.

uncertainty_samples=1000, # Number of draws for uncertainty estimation.

stan_backend=None, # Automatically select a Stan backend.

holidays_mode='additive' # Use additive holiday effects.

)

model.fit(train_prophet)

# Determine the current forecast dates from the validation set.

fc_start = i * forecast_horizon

fc_end = (i + 1) * forecast_horizon

fc_dates = valid_dates[fc_start:fc_end]

# Create a "future" dataframe with the forecast dates.

future = pd.DataFrame({"ds": fc_dates})

forecast = model.predict(future)

predictions = forecast["yhat"].values

# Retrieve the actual observed sales for these fc_dates.

actual_vals = valid_prophet[valid_prophet["ds"].isin(fc_dates)]["y"].values

# Store predictions, actuals, and the associated dates.

store_predictions.extend(predictions)

store_actuals.extend(actual_vals)

forecast_dates_list.extend(fc_dates)

# IMPORTANT: Grow the training set with the ACTUAL observed values from the validation set.

new_train = valid_prophet[valid_prophet["ds"].isin(fc_dates)]

train_prophet = pd.concat([train_prophet, new_train]).sort_values("ds").reset_index(drop=True)

store_predictions = np.array(store_predictions).tolist()

store_actuals = np.array(store_actuals).tolist()

store_mae = float(mean_absolute_error(store_actuals, store_predictions))

# Save the store-specific results.

results["Prophet"]["store_results"][store] = {

"forecast_dates": forecast_dates_list,

"predictions": store_predictions,

"actuals": store_actuals,

"mae": store_mae,

}

Calculate Errors#

all_mae = []

for store in stores:

store_mae = results['Prophet']['store_results'][store]['mae']

all_mae.append(store_mae)

avg_mae = float(np.mean(all_mae))

std_mae = float(np.std(all_mae))

results['Prophet']['aggregated_metrics'] = {

'avg_mae': avg_mae,

'std_mae': std_mae

}

pd.Series(all_mae).describe()

count 45.000000

mean 47723.386355

std 30315.527289

min 8256.784922

25% 28595.507719

50% 39556.643287

75% 63825.478654

max 149736.209768

dtype: float64

save_all_results(results)

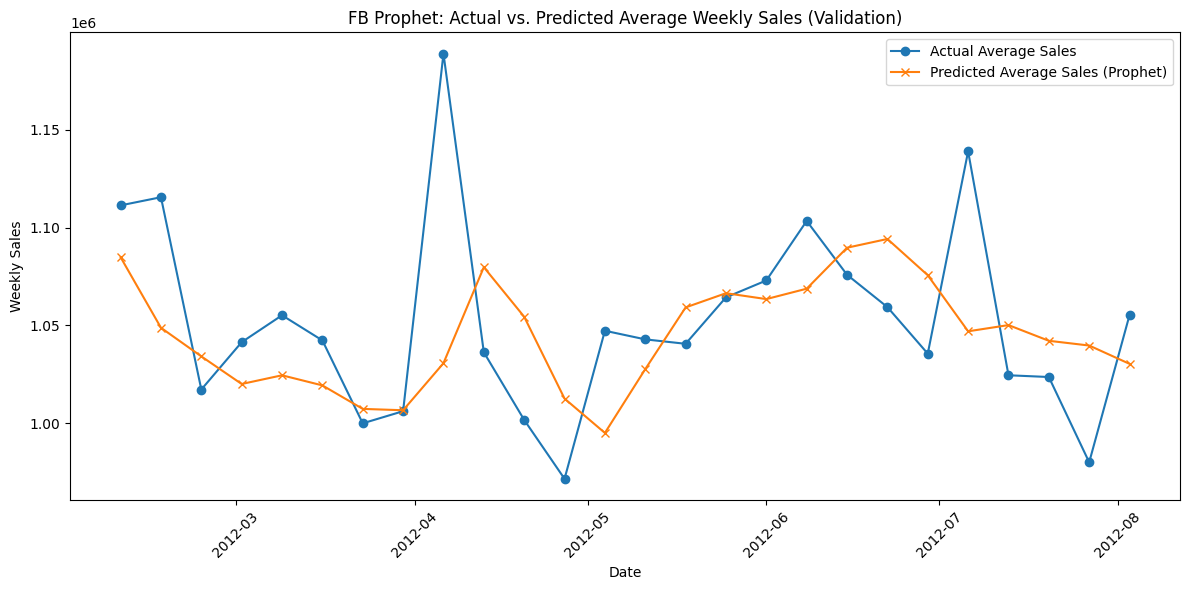

Visualize Predictions#

Show code cell source

# Aggregate predicted and actual values by forecast date across all stores.

pred_by_date = defaultdict(list)

actual_by_date = defaultdict(list)

for store in stores:

store_result = results["Prophet"]["store_results"][store]

for dt, pred, act in zip(store_result["forecast_dates"],

store_result["predictions"],

store_result["actuals"]):

# Make sure that the forecast date is a pd.Timestamp.

dt = pd.to_datetime(dt)

pred_by_date[dt].append(pred)

actual_by_date[dt].append(act)

# Sort forecast dates.

sorted_dates = sorted(pred_by_date.keys())

# Compute the average prediction and actual sales for each date.

avg_pred = [np.mean(pred_by_date[dt]) for dt in sorted_dates]

avg_actual = [np.mean(actual_by_date[dt]) for dt in sorted_dates]

plt.figure(figsize=(12, 6))

plt.plot(sorted_dates, avg_actual, marker="o", label="Actual Average Sales")

plt.plot(sorted_dates, avg_pred, marker="x", label="Predicted Average Sales (Prophet)")

plt.xlabel("Date")

plt.ylabel("Weekly Sales")

plt.title("FB Prophet: Actual vs. Predicted Average Weekly Sales (Validation)")

plt.legend()

plt.xticks(rotation=45)

plt.tight_layout()

plt.show()

SARIMA#

Separate train test split and growing windows#

# Split the 131 weeks: the first 111 weeks for training and the next 20 weeks for validation

train_dates = train_val_dates[:105]

val_dates = train_val_dates[105:]

# We will forecast in 4-week horizons over the 20 validation weeks.

forecast_horizon = 1

n_forecast_iterations = len(val_dates) // forecast_horizon # should be 20/2 = 10

random_stores = random.sample(stores, 25)

Training#

Show code cell source

results = load_all_results()

if 'SARIMA' not in results:

results['SARIMA'] = {

"store_results": {},

"aggregated_metrics": {}

}

# Define candidate non-seasonal orders for SARIMA

candidate_orders = [(6, 1, 4)] # , (6, 1, 5), (6, 2, 4), (6, 2, 5)

# Fixed seasonal order: (P, D, Q, m)

seasonal_order = (2, 1, 5, 52)

# Loop over each store

for store in random_stores:

# Filter the store’s data and sort by date

store_df = df[df['store'] == store].sort_values('date').reset_index(drop=True)

# Split the store data into training and validation based on date

train_store_df = store_df[store_df['date'].isin(train_dates)]

valid_store_df = store_df[store_df['date'].isin(val_dates)]

# Convert training data into a time series with date as index

train_series = train_store_df.set_index('date')['weekly_sales']

# -----------------------------------------------------

# Step 1: Model Selection -- Choose Best Non-Seasonal Order

# -----------------------------------------------------

best_aic = np.inf

best_order = None

# aic_bic = pd.DataFrame(columns=['order', 'aic', 'bic'], index = list(range(len(candidate_orders))))

for order in candidate_orders:

try:

with warnings.catch_warnings():

warnings.filterwarnings("ignore")

model = SARIMAX(train_series,

order=order,

seasonal_order=seasonal_order,

enforce_stationarity=False,

enforce_invertibility=False)

fit_model = model.fit(disp=False)

# aic_bic.iloc[idx]['order'] = order

# aic_bic.iloc[idx]['aic'] = fit_model.aic

# aic_bic.iloc[idx]['bic'] = fit_model.bic

# print(f"For store {store}, order {order}, AIC: {fit_model.aic}, BIC: {fit_model.bic}")

# if fit_model.aic < best_aic:

# best_aic = fit_model.aic

best_order = order

except Exception as e:

print(f"Store {store}, SARIMA candidate order {order} failed: {e}")

continue

with warnings.catch_warnings():

warnings.filterwarnings("ignore")

print(f"Store {store} -- Selected SARIMA order: {best_order}, "

f"Seasonal: {seasonal_order} (AIC: {fit_model.aic}) (BIC: {fit_model.bic})")

# -----------------------------------------------------

# Step 2: Growing-Window Forecast with Selected SARIMA Order

# -----------------------------------------------------

store_predictions = []

store_actuals = []

forecast_dates_list = []

# Start with the training series as the initial window

series_gw = train_series.copy()

# Number of forecast iterations (26 weeks / forecast_horizon weeks per forecast)

n_forecast_iterations = len(val_dates) // forecast_horizon

for i in range(n_forecast_iterations):

print(f"Forecast iteration {i+1} of {n_forecast_iterations}")

try:

with warnings.catch_warnings():

warnings.filterwarnings("ignore")

model_gw = SARIMAX(series_gw,

order=best_order,

seasonal_order=seasonal_order,

enforce_stationarity=False,

enforce_invertibility=False)

fit_gw = model_gw.fit(disp=False)

forecast_result = fit_gw.forecast(steps=forecast_horizon)

except Exception as e:

print(f"Store {store}: Forecast iteration {i} failed: {e}")

forecast_result = np.full(forecast_horizon, np.nan)

# Identify forecast dates (next 2 weeks from validation dates)

fc_start = i * forecast_horizon

fc_end = (i + 1) * forecast_horizon

fc_dates = val_dates[fc_start:fc_end]

# Get the actual values from the validation set for these dates

valid_series = valid_store_df.set_index('date')['weekly_sales']

actual = valid_series.loc[fc_dates]

# Append forecasts, actual values, and dates

store_predictions.extend(

forecast_result if isinstance(forecast_result, np.ndarray)

else forecast_result.tolist()

)

store_actuals.extend(actual.values)

forecast_dates_list.extend(fc_dates)

# Update the growing window with the actual values (simulate receiving new data)

series_gw = pd.concat([series_gw, actual]).sort_index()

# Compute store-level rmse for SARIMA forecasts

store_predictions = np.array(store_predictions).tolist()

store_actuals = np.array(store_actuals).tolist()

store_mae = float(mean_absolute_error(store_actuals, store_predictions))

# Save store results in the results dictionary

results['SARIMA']['store_results'][store] = {

'best_order': best_order,

'seasonal_order': seasonal_order,

'forecast_dates': forecast_dates_list,

'predictions': store_predictions,

'actuals': store_actuals,

'mae': store_mae

}

Calculate Errors#

all_mae = []

for store in random_stores:

store_mae = results['SARIMA']['store_results'][store]['mae']

all_mae.append(store_mae)

avg_mae = float(np.mean(all_mae))

std_mae = float(np.std(all_mae))

results['SARIMA']['aggregated_metrics'] = {

'avg_mae': avg_mae,

'std_mae': std_mae

}

pd.Series(all_mae).describe()

count 25.000000

mean 0.111026

std 0.076609

min 0.030905

25% 0.062593

50% 0.088156

75% 0.132114

max 0.345813

dtype: float64

save_all_results(results)

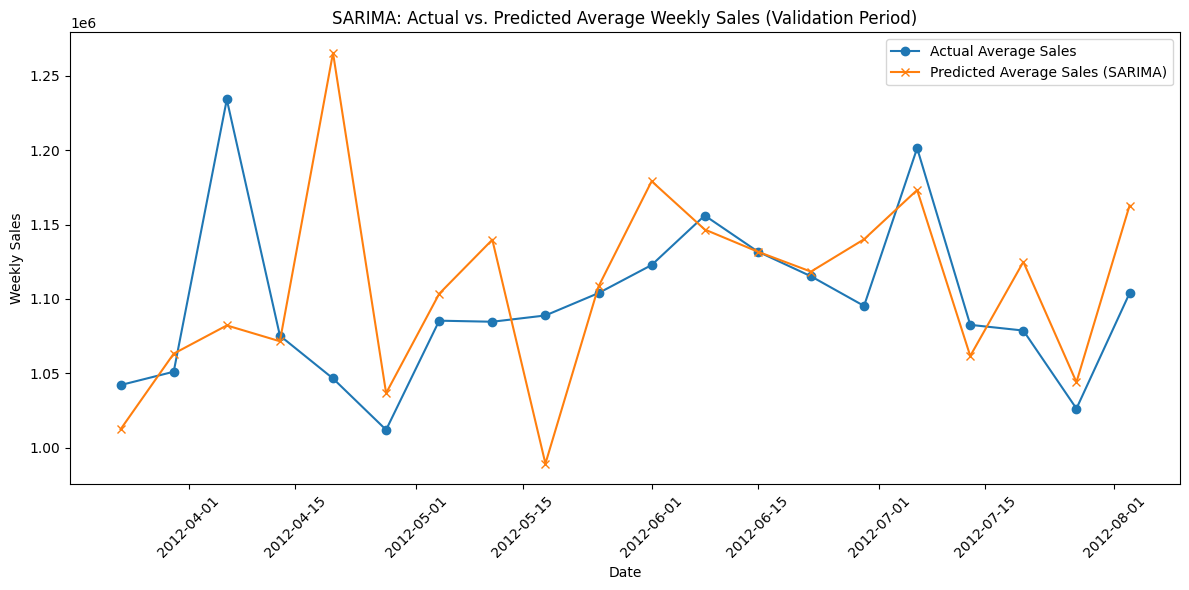

Visualize Predictions#

Show code cell source

# Aggregate predicted and actual sales by forecast date (across stores).

pred_by_date = defaultdict(list)

actual_by_date = defaultdict(list)

for store in random_stores:

store_result = results['SARIMA']['store_results'][store]

for dt, pred, act in zip(store_result['forecast_dates'],

store_result['predictions'],

store_result['actuals']):

dt = pd.to_datetime(dt)

pred_by_date[dt].append(pred)

actual_by_date[dt].append(act)

# Sort forecast dates

sorted_dates = sorted(pred_by_date.keys())

# Compute the average prediction and actual value for each date

avg_pred = [np.mean(pred_by_date[dt]) for dt in sorted_dates]

avg_actual = [np.mean(actual_by_date[dt]) for dt in sorted_dates]

# Plot the results

plt.figure(figsize=(12, 6))

plt.plot(sorted_dates, avg_actual, marker='o', label='Actual Average Sales')

plt.plot(sorted_dates, avg_pred, marker='x', label='Predicted Average Sales (SARIMA)')

plt.xlabel("Date")

plt.ylabel("Weekly Sales")

plt.title("SARIMA: Actual vs. Predicted Average Weekly Sales (Validation Period)")

plt.legend()

plt.xticks(rotation=45)

plt.tight_layout()

plt.show()

Model Comparison#

results = load_all_results()

comparison = {

'index': ['count', 'mean', 'std', 'min', '25%', '50%', '75%', 'max'],

}

for model in results.keys():

all_mae = []

for store in results.get(model).get('store_results').keys():

store_mae = results[model]['store_results'][store]['mae']

all_mae.append(store_mae)

comparison[model] = pd.Series(all_mae).describe().to_list()

comparison_df = pd.DataFrame(comparison).set_index('index').astype(int)

comparison_df

| HoltWinters | ARIMA | XGBoost | Prophet | |

|---|---|---|---|---|

| index | ||||

| count | 45 | 45 | 45 | 45 |

| mean | 42961 | 55857 | 71033 | 47723 |

| std | 26876 | 31973 | 42442 | 30315 |

| min | 9307 | 8107 | 10995 | 8256 |

| 25% | 23044 | 32722 | 35036 | 28595 |

| 50% | 37918 | 50691 | 63731 | 39556 |

| 75% | 59191 | 85070 | 98883 | 63825 |

| max | 126763 | 128366 | 194336 | 149736 |

Observations#

Comparing the mean and standard deviation of Mean Absolute errors across stores and across growing window forecasts, Holt-Winters outperforms all other models. Hence, it will be used for full forecast of the next 12 weeks.

Prophet comes in second place with slighly worse MAE scores.

Same with ARIMA, which comes in third place.

XGBoost is the worst performer with significantly higher MAE scores. However, peculiarly, when looking at the the plot of actual vs. predicted values, XGBoost would have performed extremely well if only it had predicted values one week ahead. Basically, if I shifted the predictions of XGboost by one week, it would have been the best performer.

Same case can also be observed for other models too, albeit in relatively lesser extent.

The reason behind this might be the fact that I used 52 weeks as seasonal period of 1 year. But, 52 weeks don’t completely make up 1 year. Combined with the fact that the model trained on 105 weeks (52 + 53), it might have justifyably miscalculated the seasonal effect leading to offset spikes in sales

Final Forecast#

Final Training#

Show code cell source

train_val_dates = sorted(df['date'].unique())[:-12] # first 131 weeks

holdout_dates = sorted(df['date'].unique())[-12:] # last 12 weeks

# Get the list of stores

stores = df['store'].cat.categories.tolist()

# Initialize dictionary to collect results per store.

final_results = {}

store_mae_list = []

# Also, prepare dictionaries to aggregate predicted and actual sales by date

pred_by_date = defaultdict(list)

actual_by_date = defaultdict(list)

for store in stores:

# Filter store data and sort by date

store_df = df[df['store'] == store].sort_values('date').reset_index(drop=True)

# Split the data:

# Training + Validation set (131 weeks)

train_val_df = store_df[store_df['date'].isin(train_val_dates)]

# Holdout set (last 12 weeks)

holdout_df = store_df[store_df['date'].isin(holdout_dates)]

# Set the series for training

train_val_series = train_val_df.set_index('date')['weekly_sales']

# Fit the Holt Winters model on all 131 weeks.

# Here we assume an additive model for level, trend, and season,

# with a seasonal_periods of 52 (or adjust if needed)

with warnings.catch_warnings():

warnings.filterwarnings("ignore")

try:

hw_model = ExponentialSmoothing(

train_val_series,

trend="add",

seasonal="add",

seasonal_periods=52,

initialization_method="estimated"

)

hw_fit = hw_model.fit(optimized=True)

except Exception as e:

print(f"Store {store}: Model fit failed: {e}")

continue

# Forecast the next 12 weeks in one go (non rolling)

forecast_values = hw_fit.forecast(steps=12)

# Get the actual values from the holdout set, reindex by date for comparison

holdout_series = holdout_df.set_index('date')['weekly_sales']

# Align forecast index with holdout dates (if necessary, force index order)

forecast_values.index = holdout_series.index

# Calculate error (RMSE) for the store over the 12-week holdout period.

store_error = mean_absolute_error(holdout_series.values, forecast_values.values)

store_mae_list.append(store_error)

# Save the store's forecast results.

final_results[store] = {

"forecast_dates": forecast_values.index.tolist(),

"predictions": forecast_values.values,

"actuals": holdout_series.values,

"mae": store_error

}

# Aggregate predicted and actual values per date across stores.

for dt, pred, act in zip(forecast_values.index, forecast_values.values, holdout_series.values):

pred_by_date[dt].append(pred)

actual_by_date[dt].append(act)

Error Analysis#

pd.Series(store_mae_list).describe()

count 45.000000

mean 39162.829042

std 30738.927290

min 5635.776172

25% 20474.399500

50% 32764.308580

75% 45201.375036

max 145329.783290

dtype: float64

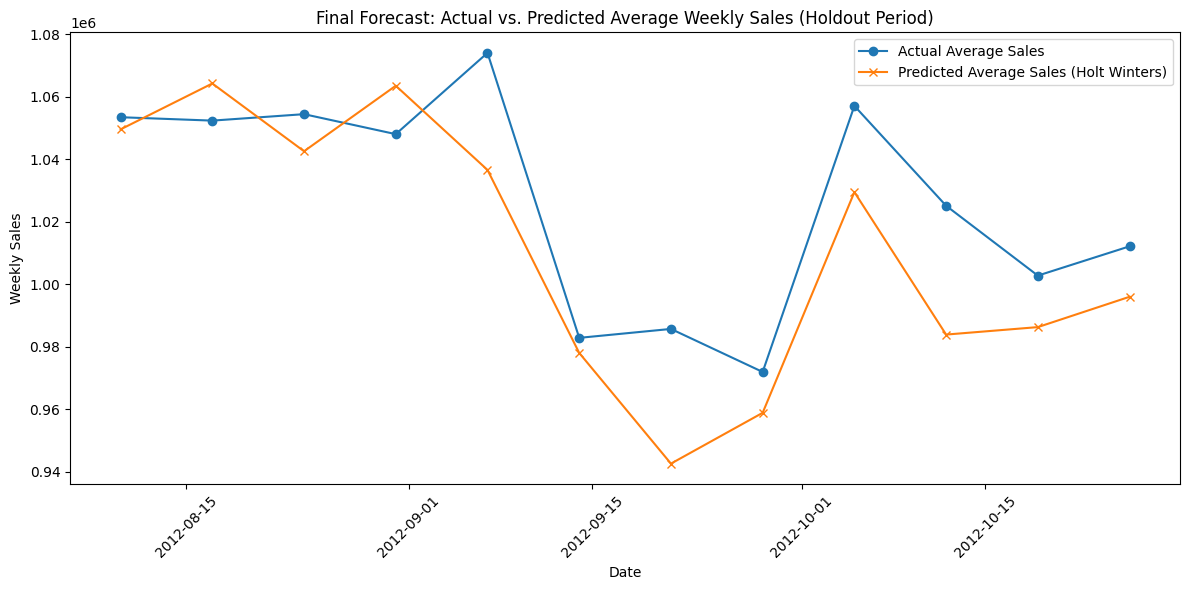

Visualization of Results#

sorted_dates = sorted(pred_by_date.keys())

avg_pred = [np.mean(pred_by_date[dt]) for dt in sorted_dates]

avg_actual = [np.mean(actual_by_date[dt]) for dt in sorted_dates]

plt.figure(figsize=(12, 6))

plt.plot(sorted_dates, avg_actual, marker='o', label='Actual Average Sales')

plt.plot(sorted_dates, avg_pred, marker='x', label='Predicted Average Sales (Holt Winters)')

plt.xlabel("Date")

plt.ylabel("Weekly Sales")

plt.title("Final Forecast: Actual vs. Predicted Average Weekly Sales (Holdout Period)")

plt.legend()

plt.xticks(rotation=45)

plt.tight_layout()

plt.show()

Observations#

As expected, Holt Winters model does predict the future sales well enough for all 12 weeks at once.

It’s average MAE for this forecast across all stores was 39162 dollars which is consistent with it’s previous average error rate calculated during model comparison using growing window forecast.

However, visual inspection shows that the model underpredicted the values 83% of times i.e. for 10 of the 12 weeks.

ToDo#

Use Darts libary’s anamoly detector + forecaster to incorporate actual ‘holidays’ events that boost sales in forecasting.

Analysze residuals. Check the Ljung-Box test for residuals.

Add another loss metric too?

Use SHAP to analyse models post training.

Create results_dict as json convertible object and save it to a file.

STL and MSTL forecasting.